The ceiling fan hums softly above as you settle onto your couch, mortgage statement in hand, mentally ticking off monthly bills. You breathe easier when you see that “mortgage insurance” line neatly tucked in… after all, it promises to protect your home if tragedy strikes. But here’s the unsettling truth: that comforting safety net is woven not for you, but for the bank. Your premiums line the pockets of the lender, and with every passing year, your coverage quietly shrinks while you continue writing the same cheque.

When you first signed your mortgage, you may have been offered or steered toward mortgage insurance, a product sold by your financial institution but underwritten by a third-party insurer. At inception, if your mortgage balance is $500,000 and your rate is $90 per month, it seems straightforward: pay your premiums, and in the worst-case scenario, your family’s home is secured. Fast forward a decade: your mortgage balance has decreased to $321,000, yet you’re still remitting $90 each month. Essentially, you’re subsidizing coverage on debt you no longer owe, with no premium relief or rebate. Worse, the beneficiary of the policy is always the bank—never you or your loved ones.

This approach lacks the long-term benefits offered by tax-efficient wealth transfer strategies or a proper estate planning for high earners.

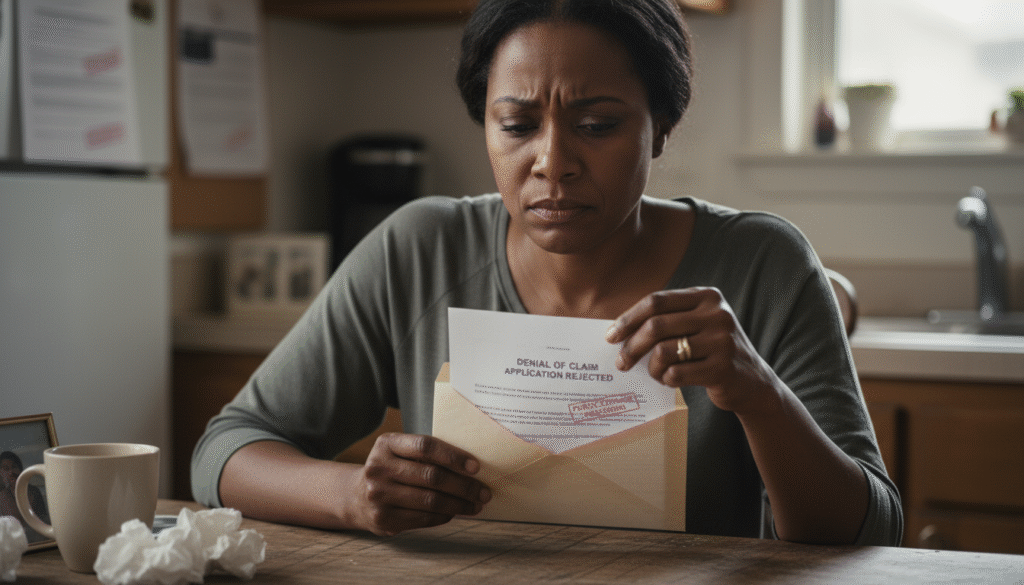

Perhaps the most insidious risk of mortgage insurance lies in when and how you’re vetted. Your lender’s financial advisor didn’t probe your medical history when they “sold” you that policy because they legally couldn’t. They merely facilitated the sale. Instead, the actual underwriting happens only if, God forbid, you die or become critically ill and attempt to claim. At that moment, the insurance company combs through your application for any omission or inconsistency: a missed doctor’s visit, an undisclosed health condition, a misremembered medication. Suddenly, what felt like guaranteed protection can be rescinded, with your premiums refunded in full and no payout to settle your outstanding mortgage.

Imagine receiving a letter months after your claim that reads, “We have determined that material information was omitted. Pursuant to policy provisions, your claim is denied.” The bank quietly forecloses on the property, and your grieving family is left shouldering a six-figure debt while the insurer pockets every premium you paid. Not exactly the “peace of mind” you signed up for.

Contrast this with a properly structured life insurance policy, whether term, whole, or universal life where underwriting happens at the outset. You complete a comprehensive medical questionnaire, undergo a paramedical exam if required, and the insurer assesses your risk before binding coverage. Once approved, your premiums and death benefit are locked in (for the term of the policy), and your chosen beneficiary stands ready to receive the full payout directly. No bank middlemen. No coverage erosion. No underwriting ambush at the moment of need.

If you purchase a 20-year term policy for $500,000 at age 40, you know exactly what you’ll pay each month and what your family will receive should the unthinkable occur. That benefit remains fixed regardless of how your health evolves, and you can rest assured that your family, not the bank, keeps the proceeds.

This is the type of forward-thinking that aligns with services offered through generational wealth coaching for millennials and family trust setup for millennials, both of which prioritize protecting your legacy.

So why do over 50,000 Canadian families still rely on mortgage insurance, placing their most precious asset and loved ones at risk? The answer lies in a perfect storm of miseducation, misaligned incentives, and the false comfort of “it’s already included in my mortgage.” Mortgage brokers and bank representatives often earn commissions for placing mortgage insurance, whereas true advice conducted by licensed advisors and brokers operates under a fiduciary standard, placing your interests front and center.

Consumers rarely pause to ask:

- Who is the beneficiary?

- What happens to my premiums as my mortgage balance declines?

- Will my claim be honored without delay?

Without these critical questions, mortgage insurance can masquerade as a no-brainer add-on when in reality, it’s a ticking time bomb that can leave families homeless and financially shattered.

At Legaciii Academy, we’ve committed to educating families about this hidden risk. Our mission is simple: keep homes in families, not banks. We teach you to ask the right questions:

- Who Benefits? Always ensure your life insurance proceeds flow directly to your loved ones, not the lender.

- Underwriting Timing: Demand upfront medical underwriting so your coverage is guaranteed when you need it, not contested at claim time.

- Coverage Consistency: Choose policies like term life or permanent life where premiums and benefits remain consistent, regardless of how your debt level changes.

- Cost-Benefit Analysis: Compare the true cost of mortgage insurance versus a tailored life insurance policy, factoring in commissions, premium duration, and benefit flexibility.

If you currently hold mortgage insurance, consider these steps:

- Review Your Policy: Examine the beneficiary clause, premium schedule, and underwriting terms.

- Obtain Quotes: Talk to an independent advisor for personalized quotes on term or permanent life coverage.

- Perform a Side-by-Side: Compare the lifetime cost of mortgage insurance premiums to a 20- or 30-year term policy of equivalent value.

- Convert or Replace: If feasible, replace mortgage insurance with a standalone life insurance policy, then cancel the mortgage insurance, securing better protection for your family.

Homeownership represents security, legacy, and the cornerstone of family life. Yet mortgage insurance, often packaged as a safety net, can leave you and your loved ones dangerously exposed. With premiums that never decrease, underwriting that occurs only at the worst possible time, and benefits paid to the bank instead of your heirs, it’s far from the peace of mind you deserve.

By understanding these hidden risks and opting instead for wealth preservation services online or properly underwritten life insurance, you take back control. You ensure that your policy works for you, paying out the full benefit to your family, at the rate and for the duration you chose. That’s real protection, real stability, and the truest way to keep your home and your legacy planning secure.