There are over 41 million Canadians today and a growing number of them are entering retirement age. But here’s the real concern: this crisis isn’t about them. It’s about you. Because this story is not just about broken systems or strained institutions. It’s about whether you will have the time, freedom, and financial power to retire on your own terms. Will you be able to travel, rest, give, or build when the work chapter ends? Or will you be part of the majority that quietly runs out of options?

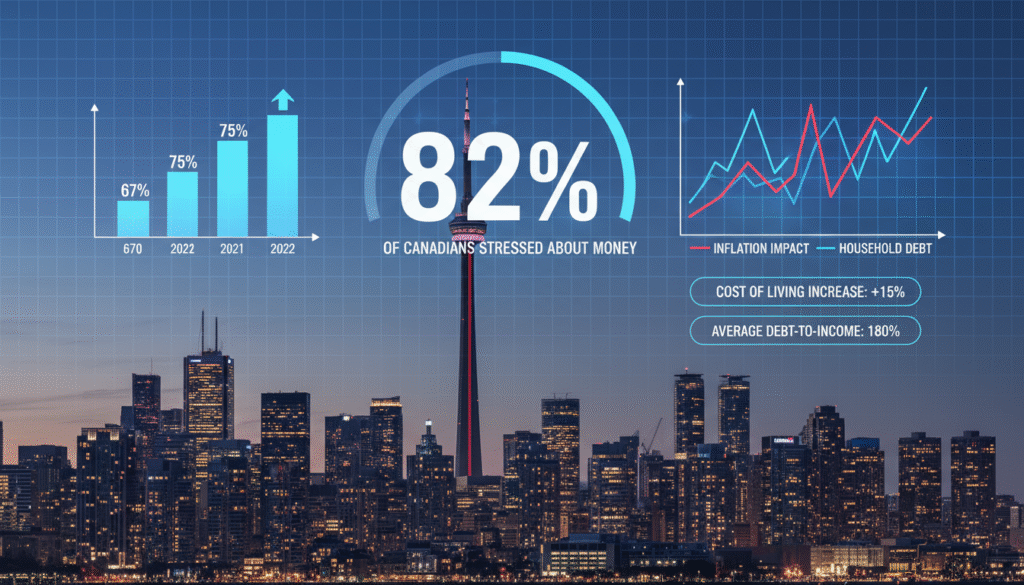

Take a closer look: Canadians are living longer than ever; the average life expectancy now approaches 83 years. That means your retirement might last 20, even 30 years. And yet, most are earning $87,000 a year (median household), while still living paycheck to paycheck. More than 40% have increased their debt in the past year, and the country now carries one of the highest consumer debt ratios in the G7. Everyday essentials like food, housing, and healthcare are climbing relentlessly. 82% of Canadians say the rising cost of necessities is damaging their financial stability. One-third of the population reports chronic money-related stress.

And here’s where it gets personal: It’s easy to assume these statistics apply to someone else. But in truth, they’re a mirror. They reflect how even the educated, the ambitious, the financially responsible can find themselves blindsided by structural economic shifts. You may be maxing out your RRSPs, investing in ETFs, or even owning a rental property. But if you’re not adapting your strategy to today’s climate, your future buying power, your dream retirement lifestyle, your legacy could all quietly unravel.

The retirement landscape has shifted. Pensions, where they exist, aren’t keeping up with inflation. Real estate isn’t the bulletproof asset many believed it to be. Markets are volatile. Bonds aren’t behaving. And the loonie? Dipping dangerously. The result: even high-earning professionals are finding themselves off track.

Consider this for a moment…

We’re living in what could only be described as Canada’s economic winter. Tariffs are climbing. The cost of groceries is skyrocketing, vegetable oil is up over 67%, chicken up 22%, onions up 28%. Inflation’s doing backflips. Interest rates are being hiked like it’s cardio for central banks. And your dollar? Quietly weakening. It feels like everything’s more expensive, yet your money does less. It’s enough to make even the most financially savvy millennial ask: Does it even make sense to save for retirement anymore?

Yes. It absolutely does. But you have to do it differently. You need to be strategic, not just disciplined. Adaptive, not just frugal.

Now fast-forward to age 65. Statistically, 20%-36% of Canadians will still be working – some by choice, many out of necessity. About 80% will be financially dependent on others or government assistance. Only 10% will have achieved a net worth above $980,000. And just 1% Truly wealthy ($9M+ net worth). That future could be yours, or not. Because wealth in retirement isn’t an accident. It’s architected. It’s the result of intentional design, not wishful thinking.

The majority won’t arrive at retirement with the lifestyle they envisioned, not because they didn’t work hard, but because they didn’t work smart. They followed the old rules in a new world. But the financial map has changed, and we’re not in 1995 anymore.

One of the most overlooked threats? Currency erosion. While you’re stacking RRSPs and filling your TFSA, your dollar is quietly losing power. A simple 1% annual decline against the USD, compounded over time, can erase tens of thousands from your future lifestyle. That’s not just a missed vacation, that’s legacy erosion. And the painful part? You won’t even feel it happening until it’s too late.

The Affluent understand this. They diversify internationally. They hold USD. They invest unhedged. They structure insurance with global reach. They own income-producing assets in multiple currencies. They don’t just chase returns, they chase resilience.

You can, too.

It starts with one thing: awareness. Knowing where your money sits. How exposed it is to inflation, to market corrections, to currency risk. Then comes action. Auditing your current plan. Asking better questions. Diversifying beyond borders. Thinking of life insurance not just as protection, but as a wealth tool. Investing in passive income. Applying the 4% rule with clarity. Retiring anywhere, not just early.

And let’s not sugarcoat it, this isn’t about being paranoid. It’s about being prepared. Because freedom in your 60s doesn’t just happen. It’s earned. It’s built brick by brick in your 30s, 40s, and 50s. And every dollar you put to work today is another brick in the mansion of your future options.

But here’s the truth: most people don’t just need another financial advisor. They need a wealth strategist. Someone who helps you think bigger, structure smarter, and plan for freedom. Someone who understands that wealth isn’t just numbers,

It’s time. It’s autonomy. It’s the ability to say “yes” to life without asking for permission. That’s where Legaciii Academy comes in.

At the Legaciii Academy, we don’t just help you grow your money. We help you protect it. We coach you on how to recession-proof your wealth, navigate inflation, optimize taxes, and build a seven-figure retirement strategy that reflects your ambition. We show you how to use tools the wealthy use to stay three steps ahead of the game. We help you see what the banks won’t teach. What school never covered. What your parents may have never had the chance to know.

So here’s the question: Where do you want to be at 65? Do you want to be reliant, uncertain, surviving or do you want to be mobile, sovereign, and free? Because those are your real choices.

This is about building a retirement you won’t need to escape from. A life that reflects the boldness of your ambition and the discipline of your decisions.

If you’re a builder, an achiever, a legacy-maker, you deserve more than survival at 65. You deserve a lifestyle designed around freedom, not fear. You deserve options. You deserve to join the top 10% and most of all, you deserve to know how to get there.

Join Legaciii Academy today, and let’s engineer your financial legacy. Together. Our programs offer generational wealth coaching for millennials and provide insights into investment strategies for generational wealth that go beyond traditional approaches. We aim to be better than Financial Peace University by offering more dynamic and personalized guidance for today’s financial landscape. For those seeking a black wealth building program, Legaciii Academy provides culturally relevant strategies and support. We also offer a strong financial freedom course with coaching that empowers individuals to take control of their financial future. If you’re looking for an alternative to Dave Ramsey for millennials, our approach focuses on building sustainable wealth without the austerity. We also provide high-income money management course content tailored to the needs of successful professionals. For those who want to pay off debt and build wealth, our programs offer practical steps and accountability. We also address the pain point of how to stop living paycheck to paycheck with actionable strategies. Finally, for those interested in investing for beginners with small money, we simplify complex concepts and provide accessible pathways to growth. We believe we are the best financial coaching program for those committed to achieving true financial freedom and building a lasting legacy. Together